1MG FlippingBooks

Funding our farmers

Simon Ville

While we may think of the energy and manufacturing industries as the capital intensive consumers of financial markets funds, farmers have required extensive financial assistance since the earliest days of colonial settlement. Simon Ville looks back at the intertwined history of the financialand agricultural industries.

Farmers’ financial needs have always been varied, from long-term capital investment (for land clearing, irrigation, building works, stocking and machinery), to medium-term assistance during cyclical downturns, and short-term trade finance to cover the seasonal lag between cropping or shearing and the sale of the commodity in overseas markets.

Lending to farmers has always been considered a risky proposition. The remoteness of farms, the need for specialist knowledge and the volatility of the market and climate have all discouraged lenders. Despite this, Australian farmers have proved to be highly successful, helping to drive the country’s economic development through the bountiful exports of many commodities – particularly wool, wheat, meat and dairy.

Behind each of these success stories is a history of sustained high rates of investment: in the nineteenth century, annual capital formation in farming represented a quarter to a half of national totals, a share surpassed only by that of residential building. After Federation and the ensuing expansion of manufacturing and services, farming’s share of national capital formation fell back to around 15-25 per cent. Intergenerational reinvestment – profits being literally ploughed back – has importantly served the expansion of many family farms over long periods of time. Nonetheless, the support of Australia’s capital market institutions has been of lasting significance in shaping our farming sector across two centuries.

Settlement of the land

The earliest rural settlers were squatters who benefited from claiming, without charge, Crown lands on which they placed sheep – self-reproducible capital that grew in numbers naturally and rapidly. However, for the squatters these apparent benefits were also challenges. They needed to build paddocks to contain their increasing flocks, a risky expenditure given no guarantee of land tenure.

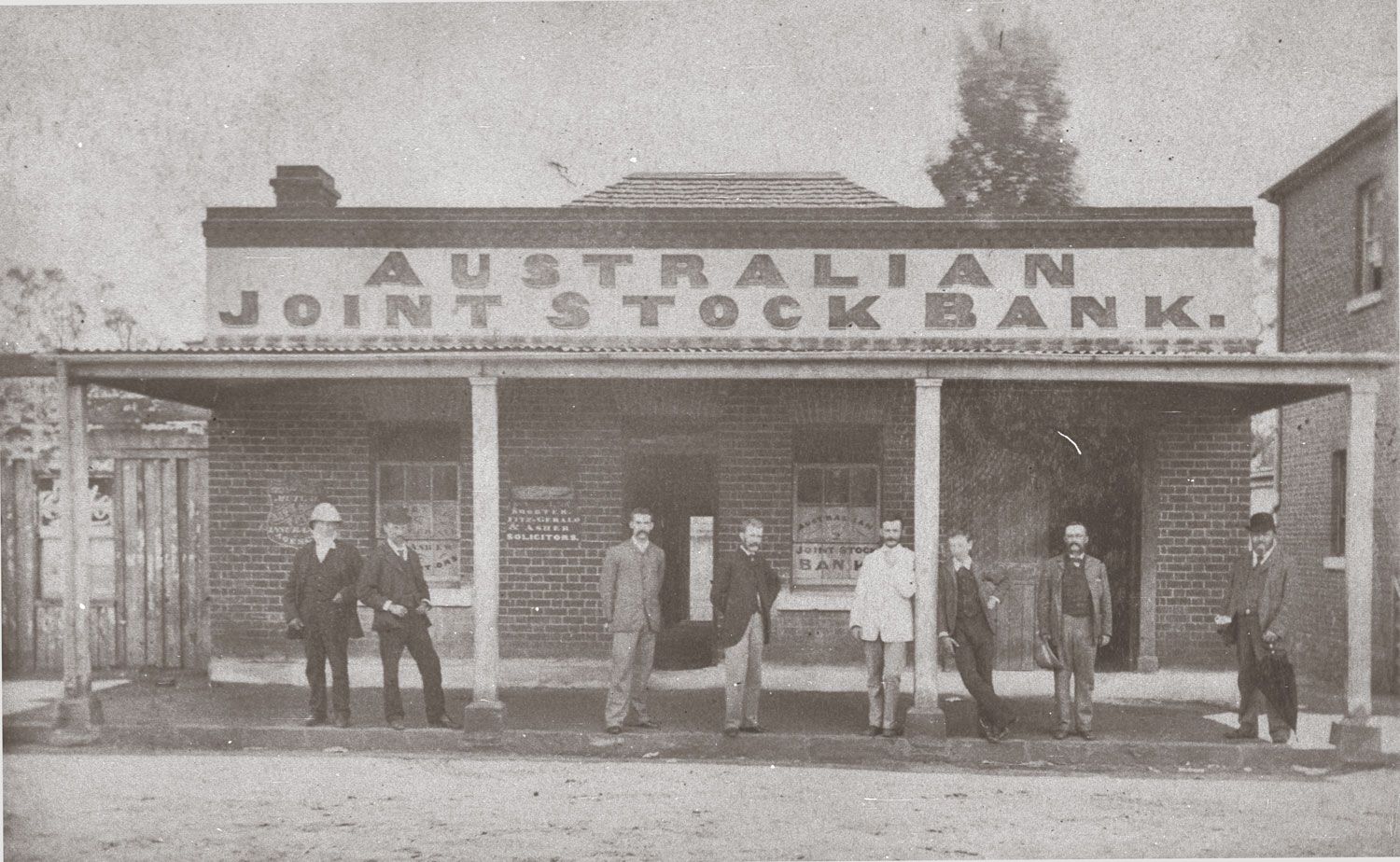

Larger flocks also necessitated looking beyond local markets to sell their wool at a time when London was the principal international auction centre for wool. British banks had begun to arrive in Australia by the 1830s – including the Bank of Australasia in 1835 and the Union Bank in 1837 – bringing with them access to British funds and mobilising local capital through branching and deposit-taking. While providing short seasonal accommodation for farmers, hopes for longer term support for capital investments were dashed by the introduction of conservative banking regulations in the 1840s as a sober response to the alleged wild economic speculations of previous decades. These measures restricted lending against property, limiting the ability of banks to support rural development through long term loans.

Help was at hand. A series of legal reforms brought squatters within the law. In 1836 squatting was legalised in return for an annual licence fee. The more vexing question of security of tenure was resolved in 1847 with pastoralists granted 14 year leases – a suitable compromise that encouraged investment but still left the door open for land reforms which, from the 1860s, redistributed some of the vast neglected squatter lands to settlers pursuing smaller scale, but more intensive, farming. Besides providing an incentive for erstwhile squatters to invest in improvements, tenure also enabled them to offer their land as loan security, which gradually encouraged banks to become more accommodating.

The rise of the stock and station agent

However, it was the rise of the stock and station agent industry (sometimes known as pastoral finance companies) which provided the financial shot in the arm that the rural sector needed.

The rapid expansion of rural production in Australia and exports out of the country, especially wool, from the mid-nineteenth century onwards provided one of the earliest opportunities for business specialisation for the burgeoning colonial economies. As we noted above, the challenges farmers faced included access to financial support and to overseas markets. Many were first-time farmers who also sought business and technical advice. The stock and station agents provided all of these services as a one-stop service for the ‘man on the land’. Many agents were themselves former farmers who were well-connected locally and recognised the need for a rural services specialist to fill this ‘entrepreneurial gap’ between farmers and buyers. These agents would set up shopfronts in their communities, and thus the ‘Rural Entrepreneurs’ came into being [Simon Ville, The Rural Entrepreneurs: A History of the Stock and Station Agent Industry in Australia and New Zealand, Cambridge University Press, 2000].

As settlers spread across the continent in the second half of the nineteenth century, every rural town became home to at least one stock and station agent. Most agents were charismatic figures who connected into rich seams of social capital in small towns and made it their business to know everyone else’s business. In addition to their many other services, agents also organised livestock auctions, major occasions in the local social and economic calendar that furthered their influence. Agglomeration through mergers and acquisitions occurred in phases, and by the late nineteenth and early twentieth centuries major national firms – household names such as Dalgety, Elders and Goldsbrough Mort – had begun to dominate the agent industry. By the 1960s there were nearly 1500 agent branches across Australia, a third of which were owned by the five largest companies.

The agents both lent to farmers directly and served as intermediaries between them and the general banking sector as these major financial institutions recognised the business opportunities presented by the growing rural sector and found ways to circumvent its regulations. Credit markets rely on accurate information to work effectively, without which loans might never occur and, if they do, could result in foreclosure. Without good information about the borrower and their business, lenders faced problems that economists refer to as ‘adverse selection’ and ‘moral hazard’, wherein the wrong people are lent to or borrowers behave dishonestly.

The agents, unlike the bankers, understood the agriculture industry and knew local farmers. Moreover, their knowledge and connections meant they often stood by their farmer clients through severe depressions when general bank lenders would cut their losses and foreclose in large numbers (as happened during the interwar downturn). Collectively agents accounted for around 12 per cent of assets in the financial intermediation sector, a portion surpassed only by that of the major banks.

Agents were able to make this strong commitment to farmers by tying their own success closely to that of their farmer clients. In return for agent financing, the farmer agreed to sell or consign their wool through that agent, who earned valuable broker commissions in return. Thus, supporting farmers through thin times wasn’t just good will; it came with the promise of valuable future commissions. Indeed, agents sometimes lent to farmers at zero profit or even at a loss in order to compete effectively against banks, which were mostly unable to provide wool commission services. Of course, not all farmers were constrained by debt obligations in choosing how to sell their clip and some were less inclined to see the long-term benefits of mutuality. As one farmer noted, ‘‘I shear the sheep, and my agents shear me” [A. Sinclair, A Clip of Wool from the Shearing Shed to Ship (Sydney, 1913), 2nd ed., p. 13.].

Subdivision, crisis and the growth of local markets

Later in the nineteenth century, new challenges emerged for lenders from the subdivision of many large pastoral estates into more diverse, smaller farms. These ventures, such as dairying and frozen meat production, were undertaken by farming families, sometimes jointly, with few resources to fall back on. Moreover, the severe drought and economic downturn of the 1890s stretched many agents as well as farmers. At least one major agent, Goldsbrough Mort, was nearly dragged under by the financial crisis of the early 1890s which gutted much of Australia’s banking industry. Goldsbrough Mort had to be reconstructed in order to survive a crisis which permanently closed the doors of half of the nation’s deposit-taking institutions.

From this near death experience emerged the cathartic realisation that agents had been making too many long-term illiquid loans to farmers while relying on relatively short-term and cyclical income flows from commodity sales and deposits at call. As a result, many agents restructured their businesses in a manner that promoted cooperation with the banking sector – leaving the banks, with their greater financial resources, to provide long-term loans while agents focussed on mediating these loans and providing mostly short- and medium-term financial support. This new business model was also consistent with a shift towards brokering wool sales, which at end of the nineteenth century began relocating from London to the Australian capital cities (especially Sydney, Melbourne, Adelaide and Brisbane).

Some banks responded to these changes by broadening the range of pastoral services they offered. A number of savings banks established rural

departments and several banks dedicated solely to agriculture emerged, particularly in Queensland, Tasmania and Western Australia. The knowledge and skills required for responsible lending to the rural sector meant that specialist providers continued to dominate through the twentieth century, either as offshoots of major banks or the products of former stock and station agencies. Among today’s leaders, Rabobank derives from Dutch agricultural cooperatives, while Rural Bank, which owns Rural Finance Corporation (a former lender for the Victorian government), is the result of an alliance between Elders and Bendigo and Adelaide Banks.

Government lends a ‘helping hand’

Governments of all political leanings have recognised the importance of maintaining a productive and prosperous farming sector. Agricultural exports have been a key source of economic growth and a means of paying for manufactured imports. The sector holds important strategic relevance, indicated perhaps in the monopsony over key commodities provided to the British government during both World Wars. A thriving Australian rural sector embodies a cultural icon for Australia by providing national identity and confidence in our place in the global economy. Atop all of this, the rise of the Country Party (the forerunner of the National Party) from the 1920s has provided a powerful political voice to farmers.

Much of government’s financial support has been designed to address the cyclical instability of farming. State governments have provided emergency assistance to farmers in hard times. In the prolonged downturn between the two World Wars, state governments intervened by using bridging finance to foster cooperative behaviour among farmers in the hope that this would be cost-reducing. Queensland passed the Primary Producers Cooperative Association Acts 1923-6 and the New South Wales government registered co-operatives under the Cooperative, Community Settlement and Credit Act.

The federal government was closely involved with funding the post-WWI soldier settler scheme to put returned servicemen on the land. Inadequate resources and plot sizes destined many of these new farmers to failure, which in turn became the business of government. In 1925, the Rural Credits department of the Commonwealth Bank – an institution increasingly behaving like a central bank – was set up to provide struggling farmers with short-term assistance.

Supporting farmers through periods of drought has been a key aspect of government support programs since the 1930s. However, policy has evolved from support designed to provide temporary assistance to more proactive measures, such as assisting farmers in drought-proofing their properties through better access to, and more efficient use of, water.

In recent decades, governments have looked more closely at how structural changes in the economy impact farmers. Changes in global markets and technological innovations, in particular, shift the competitive basis of many farming units. Structural adjustment funding has been designed to support farming units that appear to be viable beyond short-term shocks and assist the departure from the industry of others not considered sufficiently competitive to survive.

In addition to giving direct support to individual farmers, governments have intervened in volatile markets to reduce farming risks by providing greater income stability. From the early twentieth century onwards, the price of many Australian farm products was set by some form of central intervention, usually a statutory marketing board. Volatile commodity prices impact agriculture heavily due to high fixed production costs, which cannot easily be adjusted downwards in response to falling incomes. The growing class of small farmer in the twentieth century had fewer resources to fall back on than their colonial forebears, and faced unstable cycles of boom, bust and wartime imperatives.

Wool differed from most other farm products, since its heterogeneous nature made it unsuitable for sale through a marketing board. Pastoralists argued among themselves for half a century over whether to introduce a reserve price scheme that would stabilise the price of wool through thick and thin and provide greater certainty for small farmers who, by 1945, greatly outnumbered the older pastoralist elite. At length, a reserve price scheme was introduced in 1970 under which wool that failed to sell at auction above an administratively determined price would be centrally purchased under the supervision of the Australian Wool Commission. The result was the accumulation of a huge and expensive stockpile of wool, which forced the ignominious termination of the scheme in 1991. At the end of that decade, a report into the future of the wool industry was singular in its rejection of reserve price schemes:

“Under no circumstances whatsoever should any form of RPS for wool ever be reintroduced into Australia.”

The establishment of the Sydney Greasy Wool Futures Exchange in 1960 proved a more successful and enduring vehicle for stabilising farmers’ financial returns, and laid the foundation for the contemporary Sydney Futures Exchange.

Modern markets and agribusiness

A growing share of agricultural production in the last few decades has been produced by large agribusinesses. Many of these companies have expanded to meet the growing economies of scale through technically-advanced production. This has led to the point that such large agribusinesses can secure listings on the Australian stock market to benefit from the post-1980s deregulation of the Australian capital market and gain access to a range of financial instruments and institutions. Some of these businesses have expanded by combining vertical integration in the growth and transformation of farm products, or by providing the sector with services such as marketing. By the end of 2015, agribusinesses listed in Australia had a combined capitalisation of $20 billion. Elders, Nufarm and Graincorp are among the largest of these companies.

Some very large agribusinesses are foreign multinationals that have brought their funds and expertise to the local sector; these include JBS Australia (Brazilian meat business), Glencore Grain (Swiss commodity logistics) and Wilmar Sugar (Singaporean sugar refiner).

The growth of the Asian middle classes is presently seen as a major source of demand for Australian farm output in the coming decades and, more broadly, has motivated discussion about whether a boom in food production will provide the next source of national economic growth after the end of the mining boom. Funding the necessary investment to grow production has reignited the old debate of selling off the farm, as the extent to which future agricultural expansion should be funded by foreign capital is discussed across the country.

About the author: Simon Ville is Professor of Economic and Business History, School of Humanities and Social Inquiry in the Faculty of Law at the University of Wollongong. He has a BA (Hons) in History and a PhD in Economic History from University College London and has previously worked at the Australian National University, Harvard Business School, London School of Economics, and the Universities of Glasgow and Melbourne. He has also won the Bruce McComish Prize in Economic History (awarded to the best publication on the economic history of Australia and New Zealand) for his book The Rural Entrepreneurs: A History of the Stock and Station Agent Industry in Australia and New Zealand.

NEWS

After four years of customer research and 500,000 test kilometres, Ford says the Ranger Super Duty brings farmer-driven customisation into the factory, with more towing, payload, and durability built in.

StockLive runs weekly online commercial sales for cattle and sheep —

giving agents, producers and buyers a simpler, more transparent way to

trade livestock nationally.

YaraRega helps macadamia growers improve nutrient efficiency and operational flexibility through fertigation or dry application, supporting consistent tree performance, productivity, and seasonal nutrient management

The global agricultural landscape is currently weathering a perfect storm. With ongoing conflict in the Middle East and instability involving major trade routes, the supply chain for traditional synthetic fertilisers has been pushed to the brink. For Australian farmers, this isn’t just a headline, it’s a direct hit to the bottom line, with skyrocketing costs and looming shortages threatening the next harvest.

The U10 Pro Range redefines what a top‑tier full‑size UTV can be, launching a bold new era for the UFORCE family — now offered in three distinct models

Australian farmers are facing overwhelming pressure. They shouldn’t have to face this alone.